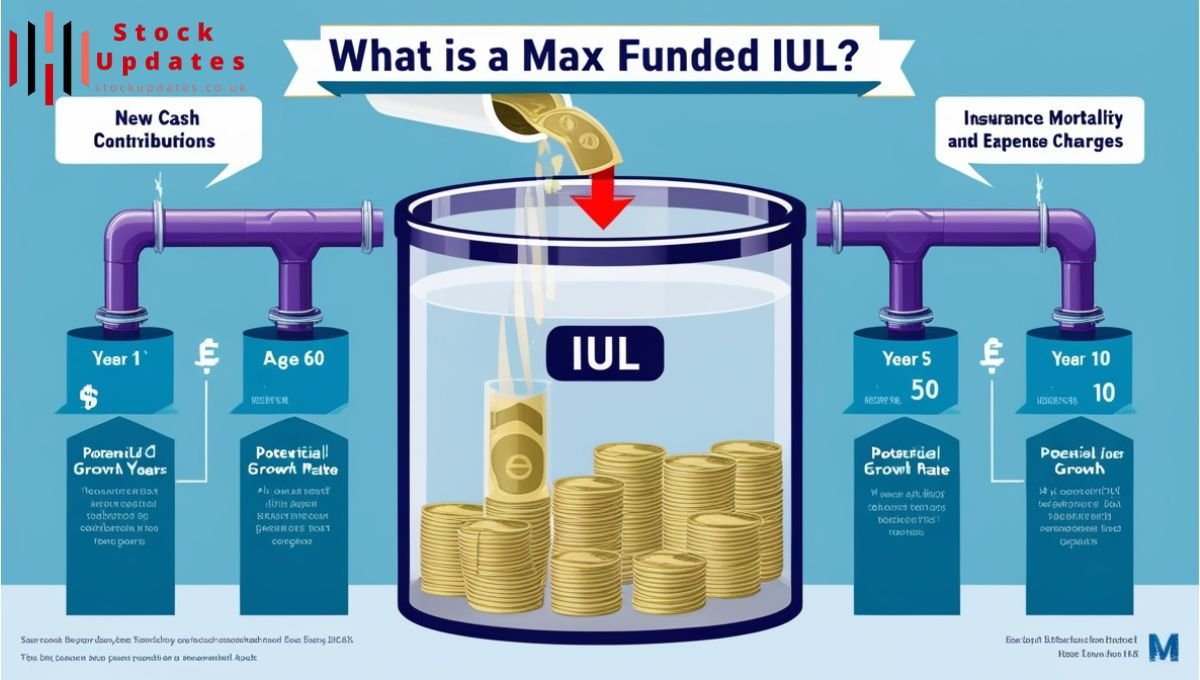

What is a Max Funded IUL

Regarding the personal financial and life insurance; one of the growing types of insurance product which is actually an insurance product, but it is also an investment product is the IUL or Indexed Universal Life Insurance., but also an investment tool. A Max Funded IUL does one better by getting as much cash value growth within the policy as is possible.

This blog post will also look at What is a Max Funded IUL is, how it operates and then discuss what can be considered the pros and cons. We will also look at who it will be advantageous for this strategy and we will provide a side by side comparison table of Max Funded IUL to other forms of investment out there for easy comparison.

What Indexed Universal Life (IUL) Insurance

There exists and insurance policy known as What is a Max Funded IUL Indexed Universal Life (IUL) Insurance which can be best described as a permanent insurance policy whereby the life assured is going to benefit from market gains directly one way or the other while market losses are simply the cost of the insurance. Indexed Universal Life (IUL) is a kind of permanent insurance that consists of high flexibility concerning premiums and death benefits, positive aspects of cash values growth.

This means policyholders get compound progression and protection from economic disaster at the same time.

What is the Significance of the MAX Funded IUL

This level of funding opportune the highest cash value growth that shall in return accumulate and grow tax-free.

How Does Max Funding Work?

To increase funding policyholders pay additional amounts not only the usual amount for premium to keep the policy active. These extra premiums pay into the policy’s cash value, which then increases over the years in relation to the chosen index. The ultimate idea is to have a good cash pool that one can withdraw tax free under some circumstances.

IUL Elements for a Maximum IUL Funding

1. Premium Payments

An extra contribution beyond the minimum is made by policyholders for reaching the highest funding limit.

2. Tax Advantages

Cash value accumulates on a tax shielded basis, and distributions, if made in the policy year that the policy is not considered a Modified Endowment Contract or MEC, are tax-free.

3. Loan Access

Permits policyholders to surrender paid-up cash value for tax-exempt loans along with reasonable loan interest rates.

By following these guidelines, policyholders can make their IUL to act as a wealth building instrument, in order to create a huge cash fund that shall remain unthreatened by any market downturns.

Benefits of a Max Funded IUL

1. Tax-Advantaged Growth

The biggest of advantage of What is a Max Funded IUL is that the policyholder can have tax-sheltered growth of cash value.

2. Downside Protection

However, unlike in the stock market, with an IUL policy the money invested in cash value is protected from fluctuations in the market,

3. Access to Cash Value

Policyholders can borrow money from the company against the policy without incurring any taxes; these usually have little effect on the death benefit available for beneficiaries. It therefore means that Max Funded IULs are a good plan for funding for retirement, education expenses or any emergencies that one may find themselves in and all this without having to dip into the retirement savings.

4. Legacy Planning

An IUL policy’s death benefit also seeks to give a lasting memory of the deceased person while catering for the remaining needs of the beneficiaries.

Can I withdraw from my IUL?

Of course, the participant may surrender the Indexed Universal Life (IUL) product, but certain consequences should be noted. Creditor policy loans and surrender diminish the face value of cash and the death benefit upon executing that policy. Also, if any of these policies is allowed to lapse, or even surrendered, there may be gains that become taxable. There are always potential drawbacks that a person may experience at the field or financial and tax losses.

Drawbacks of a Max Funded IUL

1. Complexity and Fees

In addition, they most commonly contain a myriad of charges that reduce cash value accumulation, especially in the initial period of the insurance policy.

2. Risk of MEC Classification

If overfunded beyond IRS limits, it may have to switch to a MEC although this will retain some of the policy’s tax advantages.

3. Hearing that investment

So, during years in which the market increases its combined ratio, the policy may not reflect the entire opportunity, which restricts the cash value’s growth potential in comparison with other direct market products.

4. Failure to Honor Premiums

In other words, to achieve the desire growth policyholders have to start paying higher premiums.

Max Funded IUL

Max Funded IULs can be especially appealing to those who need an umbrella of flexible savings solution that has tax benefits and comes with a life insurance component. Ideal candidates for Max Funded IULs include:

1. High-Income Earners

Desiring tax-advantaged growth with a chance at receiving tax-free retirement income.

2. Business Owners and Self-Employed Individuals

You need an alternative to 401(k) and IRA for savings and retirement in the meantime you don’t want to settle on anything rigid.

3. Individuals Focused on Legacy Planning

Anticipating both a big estate for the next generation and liquidity during the lifetime of the policyholder.

However, are not the best products for high liquidity or ready cash because due immediate returns due to initial costs and fees associated with policy setup and administration

Comparison Table: Max Funded IUL vs. Other Investment Vehicles

This will provide a quick overview of the benefits and limitations of each, highlighting where a Max Funded IUL stands out.

| Feature/Characteristic | Max Funded IUL | Roth IRA | 401(k) | Mutual Funds |

| Tax-Deferred Growth | Yes | Yes | Yes | No |

| Tax-Free Withdrawals | Yes (if structured properly) | Yes (after 59½) | No | No |

| Market Downside Protection | Yes (with floor) | No | No | No |

| Contribution Limits | IRS-imposed funding limits | Yes | Yes | No |

| Death Benefit | Yes | No | No | No |

| Liquidity | Moderate (Loans) | Moderate (Penalties before 59½) | Moderate (Penalties before 59½) | High (Market Dependent) |

| Management Fees | Moderate to High | Low | Moderate to High | Varies |

Final Thoughts

Nonetheless, to the layman, its complexities are the essence of the matter. Before going the Max Funded IUL route, financial planner or insurance specialist advice is advisable due to implications on your portfolio and taxes.

Although it cannot be termed as a universal solution, a can be a persuasive choice as it is all in one product that offers protection, tax advantage and opportunity.

Read more about market and other categories at Stock Updates.

Post Comment